Learn How to Calculate Debt Service Coverage Ratio in Real Estate

When it comes to real estate, your debt service coverage ratio is one of the key calculations lenders look at to determine if you can afford take out a loan. Learn why DSCR is important and how to calculate it.

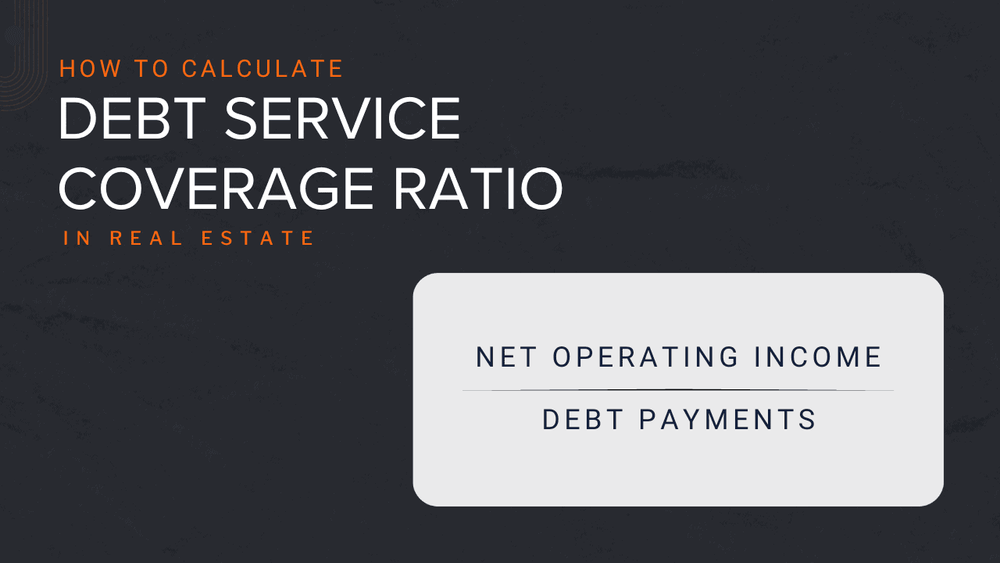

Debt Service Coverage Ratio Calculator (DSCR)

This Debt Service Coverage Ratio (DSCR) calculator allows you to determine the financial viability of a real estate investment by measuring its ability to cover its debt obligations. Simply input the property's Net Operating Income (NOI) and Total Debt Service (Loan Payments), and the calculator will automatically update to show you the DSCR and its respective status, helping you make informed investment decisions.

Ratio: 1.5

Status: Ideal

Ideal! The ratio is 1.5 or higher which is typically considered an excellent coverage in real estate.

For a more comprehensive, full-featured real estate investment calculator, sign up for Remetrics.

What is the Debt-Service Coverage Ratio?

The Debt-Service Coverage Ratio (DSCR) measures a project's ability to meet its current and future debt obligations. It can also provide insight into how much leverage a company has, and how much risk it is taking on.

In simpler terms, it calculates how much Net Operating Income (NOI) can be generated by the property to cover its interest and principal repayments.

Why is the DSCR ratio important in real estate?

Debt Service Coverage Ratio is important in real estate because it is a key financial health metric used by lenders to determine a borrower's ability to repay a loan. A high DSCR indicates that a borrower has a strong ability to repay a loan, while a low DSCR indicates that a borrower may have difficulty repaying a loan.

Debt Service Coverage Ratio Formula

The DSCR measures the amount of earnings left over after paying for all expenses, including debt service. It is calculated by dividing annual NOI by the annual debt service.

You need to know two things to calculate the debt service coverage ratio:

- Net Operating Income

- Debt Service

NOI is calculated by subtracting property operating expenses from the gross income of the property. Operating expenses are all the expenses incurred from normal business operations. Example operation expenses include repairs, property management fees, insurance, taxes, landscaping and utilities (not covered by the tenant). Gross income in real estate is the total amount of money that a property generates before expenses are deducted.

Total debt service are the debt payments - principal and interest payments - paid over a given period of time.

Generally you will want to calculate DSCR over a significant period of time. Probably a year. This accounts for seasonal changes in income and expenses. Your landscaping expenses may be different in the Fall vs the Spring, or you may have more turnovers in the Summer.

Example Calculation: Calculate the debt service coverage ratio for a rental property

- NOI: $24,000/year

- Total Debt Service: $19,672/year

Calculate the DSCR:

NOI/Debt Service = $24,000/$19,672 = 1.22

Keep in mind, we have already excluded operating expenses from rental income. 1.22 tells the investor and lender the property will generate enough net operating income to cover its current debt obligations due, plus a 22% buffer.

Good and bad debt service coverage ratios

It is important to have a DSCR calculation greater than 1. At a DSCR of 1 exactly, the property only generates enough income to pay its existing debt - no more.

A DSCR of less than 1 would be a show stopper for lenders, because NOI doesn't even generate enough income to cover its debt obligations.

The higher the ratio the better. Generally, a good DSCR would be 1.2 or higher. While 1.5 would be considered great. (source) As always, talk to your lender about the minimum DSCR they expect. Lenders want to know your project produces enough income available to pay current debt obligations and then some.

Advantages and Disadvantages of DSCR

There are a few advantages and disadvantages of the DSCR formula. Advantages include that it is a measure of a property's ability to pay back its debts, it is easy to calculate, and it can be used to compare deals. A disadvantage is that it does not take into account a company's future earnings potential.

Ways to improve your DSCR

One way to improve DSCR is to improve your net operating income, by increasing rent income and/or decreasing operating expenses. Another way is to decrease your debt payments. This can be done by refinancing your debt or by paying off your debt early. Or, by purchasing the property for less in the first place - reducing the amount of the loan.

Why DSCR changes over time

In real estate, DSCR changes over time due to changes in the overall economy, changes in the property market, and changes in the property itself.

DSCR will decrease if its interest payments increase. Thismay happen if the existing debt has a variable interest rate component, or if the investor refinances to a mortgage with a higher interest rate.

A property's DSCR will increase if its cash flow increases. Traditionally landlords increase rent slightly every year if the economy allows - improving cash flow. You could also refinance to lower interest rates.

Analyzing DSCR and beyond

Keep in mind, lenders use this ratio to determine if the property can generate enough cash flow to cover its debt service obligations. While it may be useful to the investor determine the current financial health of a property, it is more of a pass-fail situation for lenders. And, isn't all that useful unless the debt can, or needs to be, refinanced.

If you are in year 2 of a 20-year mortgage and the economy sours slightly, you should be fine as long as the property has enough cash flow available to pay the mortgage. Hopefully, economy bounces back before/if you need to refinance again.

DSCR is just one of many ratios you can use to analyze the financial viability of a property. Other important calculations include break-even ratio and return on investment. Each metric has its strengths and weaknesses. Together they help you determine how good (or bad) a deal is.